{kind=link}

How is the salary of the president of a company determined?

Hello, my name is Junpei Hamamura. He usually teaches cost accounting and management accounting at universities.

Do you know how the salaries (management remuneration, executive remuneration) of company presidents (managers, executives), etc. are determined? You may think, “Since the president is the head of the company, shouldn’t he be able to decide his own salary as he pleases?” In fact, in many companies, managers themselves decide their own remuneration, but this does not mean they are free to decide the amount.

If you are an ordinary office worker, your salary is determined based on the achievement of KPIs of your team or individual, or the tasks you are assigned, as in the recently popular “job-based employment.” Managers also have their own way of determining salary.

Advertisement

Japan’s management remuneration: “The nail that sticks out gets hammered down”

Japan has a strong sense of horizontality.

I’m sure you’re all familiar with the saying, “The nail that sticks out gets hammered down”. Roughly speaking, it means something like “If you stand out compared to others, you will be criticized.” In Japan, it is said that there is a strong sense of horizontality, as exemplified by this proverb.

In fact, in my joint research with Associate Professor Kenji Inoue of Kindai University,In Japan, the way executive compensation is determined may be significantly related to Japanese culture and customs.has come into view*1. Yes, “the stake that sticks out gets hammered down.”

Why does “the stake that sticks out gets hammered down” relate to executive remuneration? There is no point in thinking blindly, soLet’s take a look at some well-known companies.

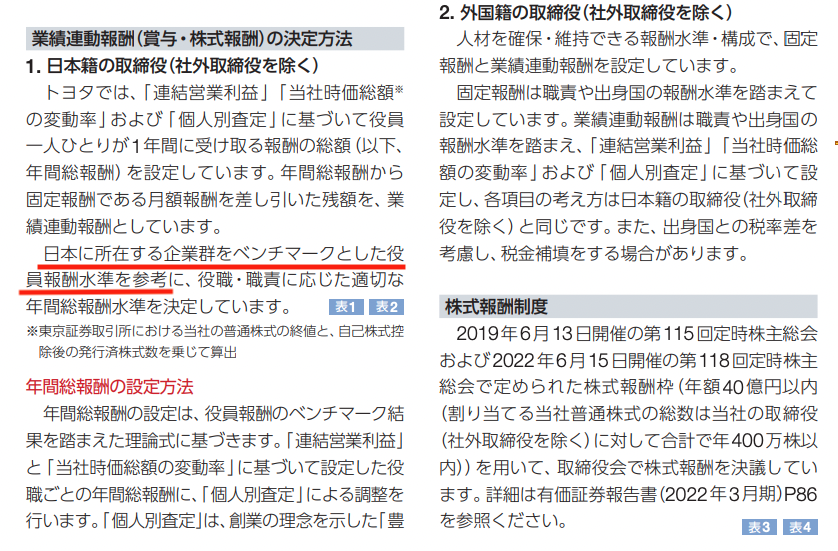

First, let’s take a look at Toyota Motor Corporation’s integrated report.Then, as one way of determining compensation,”Referring to executive compensation levels based on a group of companies located in Japan as a benchmark.”It is written.

Toyota’s integrated report states that executive remuneration is “based on executive remuneration levels that are benchmarked to a group of companies located in Japan.”

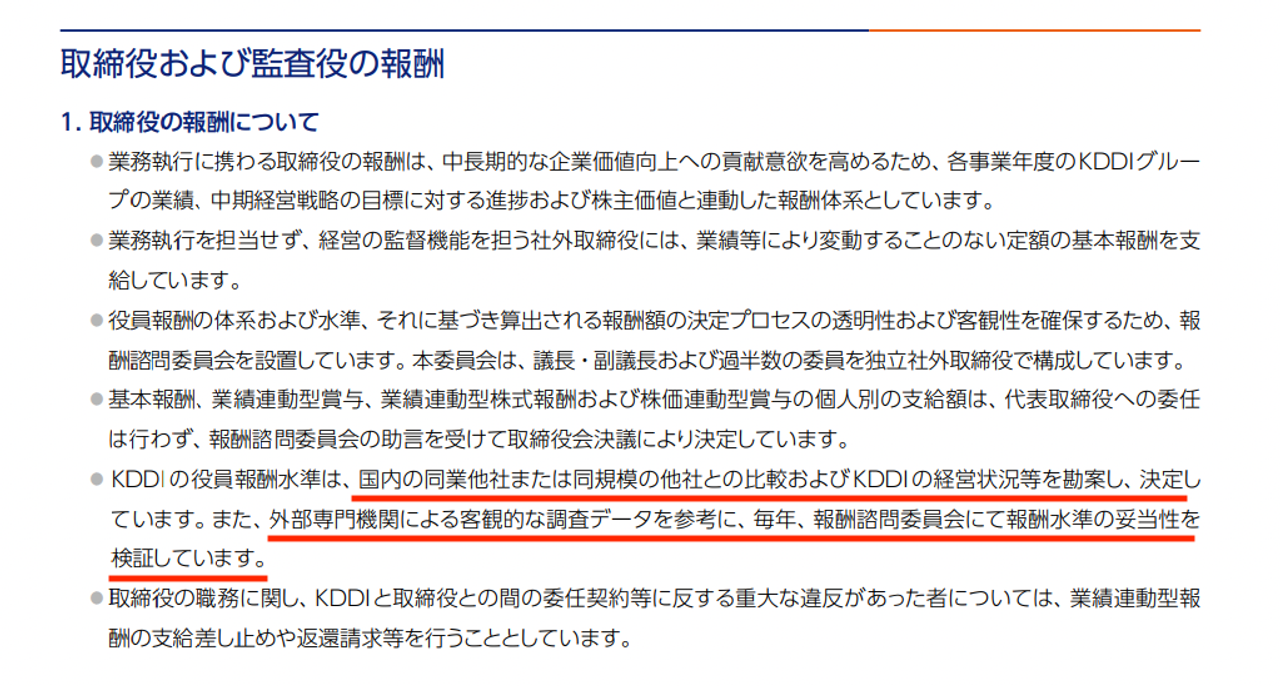

Additionally, KDDI’s integrated sustainability report states that “KDDI’s executive compensation levels are determined by comparison with other companies in the same industry or size within Japan.”Furthermore, KDDI”The remuneration advisory committee verifies the appropriateness of remuneration levels every year, with reference to objective survey data from an external specialized organization.”It also says that they are doing so.

KDDI’s last sentence gives us a suggestion. In other words,“It should be a reasonable level of remuneration.”is the importance of

When you watch the news, you may hear people criticizing management compensation for being too high. The case of Carlos Ghosn, the former Nissan Motor Company executive, is a classic example.In short, in Japan, excessively high remuneration is criticized as a “stick that sticks out”.

Companies that are conscious of this kind of “reasonable compensation level” probably don’t want to damage their reputation due to such criticism.

So, what can we do to avoid becoming a “stick that sticks out”? This is exactly what it means to “reference other companies’ compensation levels.” We refer to the remuneration levels of other companies and decide on remuneration so that it does not go too far.

The method for determining executive compensation described in the KDDI Sustainability Integrated Report.

In the US, executive compensation decreases when other companies make profits, and in Japan, it increases.

The reason we started this research was to conduct a follow-up study on executive compensation in the United States*2.

A US study points out that if companies are carefully selected for comparison, “accounting profits of other companies in the same industry” are used in executive compensation contracts. Moreover,When other companies’ profits increase, your company’s executive remuneration decreases.A relationship was observed. This is a concept called “relative performance evaluation.”Managers believe that if their company’s performance is poor compared to other companies in a similar environment, it is likely that they are not making relatively good decisions.That’s what I’m doing.

Together with Associate Professor Norimasa Ozeki of Tohoku University, we conducted a statistical investigation based on a private company database to see if the same results could be observed in Japanese companies.*3 However, in Japanese companies, even when comparing companies are selected in the same way, it was found that when the profits of other companies increase, it has a positive impact on the remuneration of the company’s executives (there is a positive correlation).In other words, when other companies make money, for some reason our company’s executive compensation also increases..

We also thought, “No, that can’t be true,” but one of the reasons we came up with while thinking about why this result happened was the example of Toyota Motor Corporation that we introduced earlier.

In other words,”As other companies’ profits have increased, executive compensation at other companies has increased, and as a result, executive compensation has also increased at companies that use that compensation to determine compensation.”It is thought that there is a possibility.

Even the same event can have different effects depending on the company.

They may also be considering the risk of being criticized for paying too high a salary when comparing it with other companies in the same industry.

By the way, in our research, we selected the comparison companies (10 companies) based on additional research. In addition to the industry and company size, the selection criteria considers “the extent to which a company’s accounting figures reflect events that occur in the world.”

I think the industry knows this intuitively. Company size is used to compare companies of similar size. Last”To what extent do a company’s accounting figures reflect events that occur in the world?”It’s hard to understand, so I’ll explain it a little.

How companies react to events in the world and how this is reflected in their accounting figures (sales, profit and loss, etc.) differs from company to company even within the same industry. For example, let’s say the price of potatoes has risen in the restaurant industry. At this time, curry shops are directly affected by the rising price of potatoes, causing costs to rise. However, gyudon restaurants are not affected as much by the rise in potato prices, and their accounting figures do not reflect this. In other words, even within the same restaurant industry, an event such as a rise in the price of potatoes has a different impact on accounting numbers.

To take this into account, an indicator that measures the extent to which certain events in the same industry are reflected in accounting figures is called “comparability” in financial reporting.

If other companies in the same industry calculate similar accounting figures for a certain event, those companies are considered “similar companies.” Based on this, our research selected companies with high comparability and statistically investigated how executive compensation is determined.

As an aside, there is research showing that Japanese companies often use accounting figures to determine executive compensation*4. Therefore, the comparability of financial reports is a useful indicator when considering executive compensation in Japanese companies. The selection of comparison companies is discussed in more detail in Chapter 15 of “Practical Management Accounting Evidence” (Chuokeizaisha), so please read it if you are interested.

In our research, we selected and investigated comparable companies in this way, and found thatAmong listed Japanese companies, when the performance of comparable companies during the same period was at a high level, there was a tendency for the company’s executive remuneration to be at a high level as well.That’s why *3.

It’s not that “it’s bad because they’re side by side”

The impact of flattening compensation is manifold.

I think there are a variety of opinions regarding the flattening of executive remuneration. For example, there is the opinion that “If we work side by side, we can receive a certain amount of reward without having to work hard.”

Certainly, if the compensation level is the same as that of other companies, managers will have less reason to work hard because they are guaranteed the amount they will receive without having to work hard. However, on the other hand, since you are guaranteed a certain amount of compensation, there is also the benefit of being able to do something drastic. Also, since excessive compensation does not occur, if the amount paid to managers is saved, the company will have a little more money to use for other things (investments, etc.).

Also,In some cases, companies simply have a horizontal mindset of “not making compensation stand out” and do not use other companies’ compensation as an indicator.. For example, Nichirei’s integrated report states that compensation is determined based on the “compensation levels of companies that compete with our group in terms of business and human resources, including in the food and logistics industries.” In other words, it is true that companies determine their own compensation based on the compensation levels of other companies, but the reason for this is likely to be to “secure excellent human resources.”

The only thing that can be observed through statistical analysis is that in Japan, there is a tendency for there to be a relationship between compensation at one company and compensation at another company.

However, in this case as well, the amount may be criticized if it exceeds the standards of other companies. Therefore, it may be difficult to achieve extremely high rewards. The culture of “the nail that sticks out gets hammered down” may have an influence here as well.

The Company Law, which was revised in 2019 and 2021, requires more detailed disclosure regarding the policy for determining executive compensation.

However, not all companies disclose this information. There are reasons why companies have not yet disclosed their information. I don’t know whether that’s because they don’t want to disclose it or because there’s nothing that can be disclosed in the first place (the compensation contract hasn’t been determined in detail). If the latter is the case, I hope that looking at trends at other companies will be of some help in designing your own compensation.

Additionally, it is important to note that the content of this article is only one factor in determining executive compensation. Of course, profits and sales are sometimes used when determining executive compensation. Additionally, please note that our paper is a preprint and has not yet passed peer review.

Junpei Hamamura: Associate Professor, Faculty of Business Administration, Momoyama Gakuin University. He graduated from the Department of Business Administration, Faculty of Business Administration, Kobe University, and received his doctorate (Business Administration) from the Graduate School of Business Administration, Kobe University. Current position since 2020. His specialty is management accounting and cost accounting. His books include “Management Accounting for Oligopolistic Competitive Enterprises” (Chuokeizai-sha) and “New Edition of Introductory Accounting (3rd Edition)” (co-author, Chuo Keizai-sha).

References

*1: Hamamura, J., and K. Inoue. 2023. The nail that stands is hammered down: Using financial reporting comparability to set peer groups on benchmarking for managerial compensation in Japan. Available at SSRN: id 4398675.

*2: Nam, J. 2020. Financial reporting comparability and accounting-based relative performance evaluation in the design of CEO cash compensation contracts. The Accounting Review 95(3): 343-370.

*3: Kenji Inoue, Norimasa Ozeki, and Junpei Hamamura. 2021. “Comparability of financial reports and relative performance evaluation: Supplementary examination of Nam (2020)” Accounting Science e2021(2): 1-5.

*4: Iwasaki, T., S. Otomasa, A. Shiiba, and A. Shuto. 2018. The role of accounting conservatism in executive compensation contracts. Journal of Business Finance & Accounting 45(9-10): 1139-1163.

Yutaka Kato, Eisuke Yoshida, and Kohei Arai (eds.), Evidence of Management Accounting for Practical Use, Chuo Keizai-sha.

(Edited by Takashi Mitsumura)

Source: BusinessInsider

Emma Warren is a well-known author and market analyst who writes for 24 news breaker. She is an expert in her field and her articles provide readers with insightful and informative analysis on the latest market trends and developments. With a keen understanding of the economy and a talent for explaining complex issues in an easy-to-understand manner, Emma’s writing is a must-read for anyone interested in staying up-to-date on the latest market news.